By

By - 181

03 Jul 2026

Trending News

-

OpenAI Jalapeño Chip, Anthropic Data Heist, and South Korea's $576B Mega-Investment

-

The Family Man Returns, Mid-Year Box Office Winners, and Cocktail 2 Strikes Gold

-

The Agentic Web, ChatGPT New Memory, and AI Shocking Environmental Cost

-

US and Iran Halt Strikes Ahead of Doha Talks as Lebanon Truce Wobbles

-

Ireland Seals Historic 2-0 Sweep Over India in Final-Ball Thriller

-

Anthropic Export Ban Eased, GPT-5.6 Previews, and Gemini Deep Think

-

Retaliatory Strikes Threaten US-Iran Deal While Israel and Lebanon Sign Framework

-

The 2026 Wellness Guide for the Screen-Bound Professional in Ghaziabad

-

Why Agentic Workflows are Triggering a Corporate Collaboration Crisis

-

Tensions Spike in the Strait of Hormuz, UN Pauses Evacuations, and Ceasefire Strains in Lebanon

-

The Environmental Toll, Bioweapon Warnings, and the Agentic Era

-

India Takes on Ireland as Shreyas Iyer Leads and History Awaits

-

Gemini Spark Launches, ChatGPT Loses Dominance, and the Threat of Agentjacking

-

The Rise of the Agentic Reputation Engine 2026 Most Profitable Micro-SaaS Idea

-

US-Iran Peace Talks Advance, Israel Holds the Line in Lebanon, and Ukraine Strikes Crimea

-

Shah Rukh Khan Nostalgic Return, Welcome to the Jungle Reviews, and Major PlayStation Layoffs

-

Workforce Readiness Drops, EU Pushes for Sovereignty, and the Agentic Era Takes Hold

-

15-Year-Old Vaibhav Sooryavanshi Set to Shatter Sachin Tendulkar Debut Record

-

Preity Zinta Takes on Big Tech, Alpha Trailer Ignites the Internet, and Taylor Swift Makes History

-

Beating the Noida Heatwave - Essential Health and Safety Tips for June 2026

-

AI Governance Takes Center Stage G7 Summit Pledges, US Executive Actions, and Agentic AI at VivaTech

-

US-Iran Sign Peace Deal, Ukraine Strikes Moscow, and the Deadly Ceasefire in Gaza

-

India Crushes Afghanistan to Seal Series as Mandhana and Bavuma Make TIME 100 Most Influential List

-

White House Executive Orders, the Pentagon AI Push, and Agentic E-Commerce

-

Shubman Gill and Ishan Kishan Demolish Afghanistan in the 2nd ODI

-

The Agentic Era and Mega-Acquisitions: Top AI Innovation News

-

The Rise of the Agentic Automation Agency - 2026 Most Profitable AI Business Model

-

Fable 5 Pulled Offline, SpaceX $60B Acquisition, and the Surging Value of AI Skills

-

How AI-First Agencies Are Dominating Local SEO and Web Automation in 2026

-

Karan Johar Malayalam Debut, Lagaan Extends Its Re-Release, and Peddi Dominates the Box Office

-

G7 Summit Begins in France, Historic US-Iran Deal Reached, and UK Bans Social Media for Under-16s

-

Shreyas Iyer Takes the Helm, a 15-Year-Old Prodigy Emerges, and ODI Dominance Against Afghanistan

-

Surviving the June 2026 Heatwave and FIFA Late Nights - Essential Daily Health Tips for India

-

Israel and Iran Shatter Ceasefire with Major Strikes as Global Oil Crisis Deepens

-

Bollywood Box Office Clashes, Alpha Big Teaser, and Amitabh Bachchan Tech Nostalgia

-

IBM Warns of Massive AI Control Gaps While UN Sounds Alarm on Environmental Impact

-

Gemini-Powered Siri and Multi-Model Intelligence Headline WWDC 2026

-

Meta Launches Meta One AI Subscriptions Across Instagram, Facebook, and WhatsApp

-

Ram Charan Peddi Sets Global Records with a Staggering Rs 135 Crore Day 1

-

How Microsoft Work IQ and Snowflake New Data Agents Unlock a Lucrative B2B Integration Business

-

Hezbollah Rejects Lebanon Truce After Deadly Tyre Strikes While Zelenskyy Demands Direct Putin Talks

-

Google Launches Gemma 4 12B to Champion Native Encoder-Free Multimodal Architecture

-

Microsoft Unveils Scout and OpenClaw Integration to Revolutionize Long-Running Enterprise Agents

-

Sensex and Nifty Bounce Back as India VIX Plummets and Government Announces Historic PPI Shift

-

Kohli Injury Blow, Surya Captaincy Shocker, and SAFF Football Final Glory

-

FWICE Drops Ranveer Singh Don 3 Ban as Ranvir Shorey Blasts Producers Guild Over Double Standards

-

Why Local AI Implementation Agencies Are the Most Profitable B2B Opportunity in 2026

-

How Vertical Multi Agent Micro-Squads are Redefining B2B AI Architecture in 2026

-

US-Iran Escalation Hits Kuwait Airport as House Reins in Trump Over Middle East Conflict

-

Alphabet $84.75 Billion AI Fundraiser Signals a Massive Shift to Autonomous Enterprise Agents

-

Google Cloud and MWM AI Introduce the Revolutionary AI Mobile Squad

-

The Top 4 Groundbreaking Tech Innovations Unveiled at Computex 2026

-

Bollywood Icon Slams Filmmakers with Stern Legal Notice Over Blackbuck Case Movie

-

Vashu Bhagnani Sues David Dhawan Over Biwi No. 1 Songs in New Film

-

Embracing Functional Fitness, Digital Wellness, and Proactive Care

-

Fragile US-Iran Ceasefire Hangs in the Balance as Strikes Resume and Ukraine Pleas for Air Defense

-

The Final Toy Story 5 Trailer Drops Ahead of Highly Anticipated June Release

-

AI Tech Boom Propels South Korea Past India as Dalal Street Faces Extreme Volatility

-

Essential Tips for Navigating Ebola, Hantavirus, and Emerging Outbreaks

-

Massive Russian Strikes Devastate Ukraine Amid Fragile Middle East Truce Efforts

-

Nvidia Unveils the Vera Rubin NVL72 Supercomputer at Computex 2026

-

Escalating US-Iran Tensions and the Ripple Effects Across the Middle East and Ukraine

-

How AI and Smart Hydration Are Revolutionizing Summer Health

-

A Historic Leap for India: ISRO Successfully Launches the Manned Gaganyaan Mission into Orbit

-

Europe New AI Engine SoftBank and Sesterce Launch Massive 1 GW Data Center in France

-

ECB and IMF Warn of Extreme Market Volatility Amidst Middle East Ceasefire Tensions

-

World No Tobacco Day, Early Cancer Screening, and Daily Vitality

-

Global Health Alerts for Navigating Ebola, Measles, and Hantavirus Outbreaks

-

U.S. Declares Readiness to Resume Iran War Amid Tense Ceasefire Talks

-

Why Hyper-Personalization and Active Recovery Are the Ultimate Health Tips

-

The Historic $65 Billion Funding Round That Reshaped AI in May 2026

-

Gujarat Titans Storm into IPL 2026 Final Shubman Gill Century Eclipses Sooryavanshi Heartbreak

-

Why AI Inference Infrastructure is the Billion Dollar Startup Idea of 2026

-

Infineon and NVIDIA Breakthrough in Next-Gen Server Architecture

-

The Mandalorian and Grogu Shatters Global Box Office Records

-

Why Hyper-Niche Co-Pilots Are 2026 Most Profitable Business Idea

-

Navigating Global Health Alerts and Elevating Your Everyday Wellness

-

Russian Drone Strikes NATO Territory as U.S. Iran Ceasefire Hangs in the Balance

-

The Rise of Vaibhav Sooryavanshi a 15-Year Old Prodigy is Redefining IPL 2026

-

Sooryavanshi Powers Rajasthan Royals IPL 2026 Qualifier 2 SRH Eliminated

-

Mitsubishi Chemical Accenture Joint Venture AI Transformation

-

Sovereign Quantum Race Accelerates Global Commitments Forty Two Billion

-

Global Markets Tread Cautiously Geopolitical Tensions Energy Supply

-

Semiconductor Surge Pushes Tech Giants Past Trillion Dollar Milestones

-

Staying Vigilant Public Health Guidance Global Ebola Advisories

-

Geopolitical Strains Deepen Long Range Strikes Peacekeeping Deadlocks

-

Global Markets Navigating Geopolitical Volatility Commodity Flux

-

The Agentic Shift How Googles New Gemini 3.5 and Spark are Redefining Enterprise and Consumer Tech

-

Gulf Brinkmanship Diplomatic Shifts Self Defense Strikes Iran US

-

Global Markets Rebound Crude Prices Ease US Iran Negotiations

-

HBO Max Unveils Ambitious 2026 Slate Harry Potter House of the Dragon

-

Global Energy Relief Crude Prices Plunge US Iran Diplomatic Progress

-

Netflix Confirms Emily in Paris will Officially end with Season 6

-

Escalation and Exercise Unprecedented Drone Warfare and Nuclear Drills

-

Generative AI Designs Novel Nano-Materials to Purify Drinking Water from Toxic Forever Chemicals

-

Dual Fronts Escalate Deep Range Drone Strikes Russian Energy Middle East Tensions

-

UN Cuts India 2026 GDP Growth Forecast to 6.4% as Domestic Core Sector Resurges to 1.7%

-

Search Giant Unveils Watershed AI Framework to Automate Global Travel Reservations

-

Top 3 Operational Business Tips to Scale Efficiency and Build AI-Augmented Workflows in 2026

-

4 Vital Habits to Shield Your Body and Boost Immunity Naturally

-

Sensex Recoups 1135 Points from Intraday Crash as Rupee Hits Historic Low of 96.39 Against USD

-

Sensex Recoups 1135 Points From Day Lows as SEBI Chief Assures Financial Ecosystem Resilience

-

Middle East Conflict Escalates UAE Nuclear Plant Drone Strike

-

detroit-pistons-force-game-7-cavaliers-eastern-conference-semifinals-2026

-

China Orders 200 Boeing Jets: Aviation Winners & Losers 2026

-

Suriya Action Epic Eyes Massive 25 Crore Saturday Jump as Tara Sutaria Stuns at Cannes 2026

-

INR Breaches 96 Mark Against US Dollar Amid Global Crude Oil Surge and West Asia Conflict

-

Scientists Discover Crucial Brain Nutrient Deficit Fueling Chronic Stress and How to Fix It

-

Finn Allen Explosive 93 Fires KKR to Vital 29-Run Victory Over Gujarat Titans at Eden Gardens

-

Trump Exposes BRICS Splits Over Iran War as Israel-Lebanon Truce Holds Despite Fresh Strikes

-

1 Lakh Tech Jobs Gone, But Nvidia CEO Insists Software Engineers Are Busier Than Ever

-

Mitchell Marsh Masterclass and Akash Singh Strategic Spell Dent CSK Top-Four Hopes

-

How a New Microscopic Blood Vessel Test Changes Early Heart and Kidney Detection

-

Benchmark Yields Surge to Yearly Highs as War-Driven Inflation Spooks Investors

-

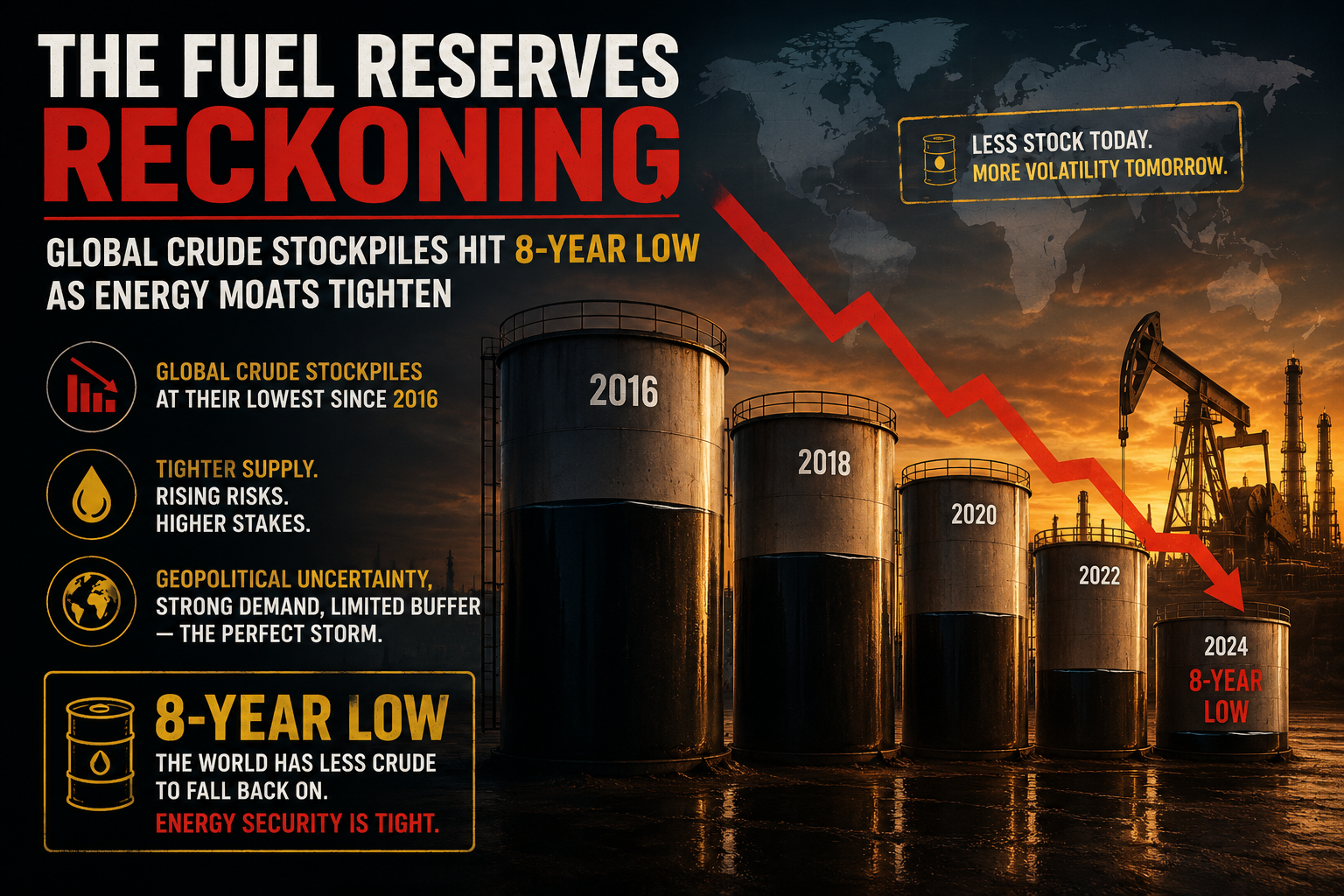

Global Crude Stockpiles Hit 8-Year Low as Energy Moats Tighten

-

Mouni Roy and Suraj Nambiar Announce Shocking Divorce After Four Years of Marriage

-

Iran Restricts Passage to Enemies as Seized Cargo Ships Pivot to Tehran

-

Google I/O Unveils Android 17, Smart Glasses, and Autonomous AI Agents

-

Kohli Smashes 9th Century as CSK Face Must-Win Clash Against LSG at Ekana

-

Why Restoring Your Nervous System is the Ultimate Health Tip

-

Rupee Breaches 96 Per Dollar Mark as Global Bond Yields and Oil Prices Surge

-

Suriya and Trisha Starrer Overcomes Last-Minute Cancellations to Trigger Theatre Frenzy

-

Experian and ServiceNow Partner to Launch Autonomous AI Agents for Global Enterprise Workflows

-

Global Markets Explode: Dow Reclaims 50,000 as Trump-Xi Beijing Summit Sparks Massive Relief Rally

Business

The global energy sector has officially entered a critical window of vulnerability that is poised to rewrite corporate operational costs for the remainder of the fiscal year. According to updated data from S&P Global Energy and prominent Wall Street institutions, global crude oil reserves have plummeted to their lowest levels in eight years. For months, the true economic impact of maritime blockades and shipping bottlenecks was partially hidden because nations aggressively dipped into their emergency stockpiles. Now, as those accessible buffers rapidly empty, energy analysts are warning that an "inevitable market reckoning" is rapidly approaching.

The Deep Drain on Global Stockpiles

When maritime routes through key chokepoints like the Strait of Hormuz faced severe operational disruptions earlier this year, a massive gap emerged between global supply and demand. To prevent oil prices from immediately skyrocketing into triple digits, countries relied heavily on their strategic reserves. In April alone, global crude stockpiles were drawn down by a staggering 200 million barrels—averaging a drain of roughly 6.6 million barrels per day.

While the world holds nearly 8 billion barrels of crude in theoretical reserves, JP Morgan estimates that only about 580 million barrels are easily accessible to the market right now. Goldman Sachs recently sounded the alarm, noting that the global economy currently has only 45 days of refined product supply left in stock, prompting a stark warning that "the worst of the crisis is ahead of us".

Domestic Fractures and Retail Price Shock

The macro-level depletion is translating into immediate, painful adjustments at the consumer level. In a direct response to these soaring wholesale procurement pressures, oil marketing companies are no longer absorbing the losses. Effective today, retail petrol and diesel prices have been slapped with a sharp hike of Rs 3 per litre to offer partial relief to state-run distribution hubs.

+------------------------+--------------------------+-----------------------------------+

| Energy Metric | Current Status / Level | Immediate Business Implication |

+------------------------+--------------------------+-----------------------------------+

| Global Crude Stockpile | 8-Year Historic Low | Highly volatile pricing models |

| Refined Product Buffer | 45 Days of Supply Left | Looming jet fuel & transport gaps |

| Domestic Fuel Price | Increased by Rs 3/Litre | Rising "Cost to Serve" logistics |

+------------------------+--------------------------+-----------------------------------+

This domestic price shock is expected to ripple across supply chains, elevating the "cost to serve" across manufacturing, freight operations, and e-commerce logistics. Leading market strategists warn that if current shipping disruptions persist, fuel prices may realistically need to climb an additional Rs 15 per litre to balance out the severe global supply squeeze.

The Structural Supply Disruption Moat

What makes this situation highly challenging for enterprise planning is that the disruption is proving to be structural rather than temporary. Commercial traffic through alternative maritime routes has bottlenecked, adding 10 to 14 days of additional transit time for vessels navigating around Africa. These delays, combined with soaring freight insurance premiums, are forcing corporate leaders to restructure their inventory management away from "just-in-time" models toward high-security asset storage.