By

By - 109

Finance

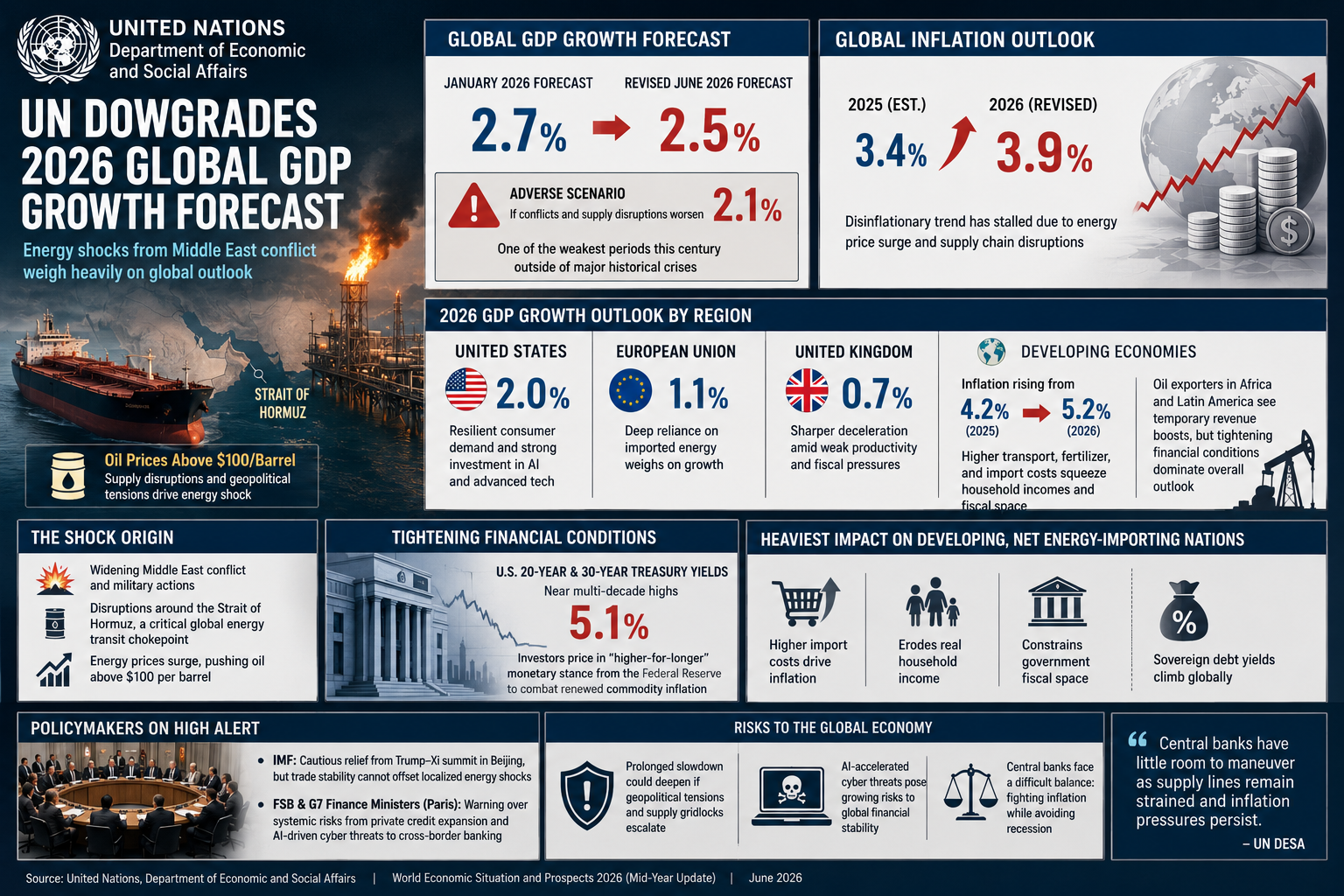

The United Nations Department of Economic and Social Affairs (UN DESA) officially downgraded its 2026 global gross domestic product (GDP) growth forecast to 2.5%, a noticeable drop from the 2.7% expansion projected in January. Released in its mid-year World Economic Situation and Prospects report, the revision stems directly from the widening conflict in the Middle East and its subsequent energy shocks. Recent military actions and disruptions surrounding the Strait of Hormuz—a crucial artery handling a significant portion of global petroleum and natural gas transit—have pushed oil prices firmly above the $100 per barrel threshold. UN economists warned that if these supply chain gridlocks and geopolitical hostilities worsen, global expansion could deteriorate to an adverse scenario of 2.1%, which would rank among the weakest periods for economic output this century outside of major historical crises.

This disruption has effectively halted the global disinflationary trend that central banks have carefully managed since late 2023. Worldwide inflation projections for 2026 have been adjusted upward to 3.9%, complicating the policy trajectories for major central institutions. The impacts, however, are diverging sharply by region. In developed markets like the United States, growth remains relatively insulated at a projected 2.0% due to resilient consumer demand and aggressive corporate investments in advanced technologies like artificial intelligence. Conversely, the European Union is facing immediate headwinds from its deep reliance on imported energy, dragging its 2026 growth outlook down to 1.1%, while the United Kingdom faces an even sharper deceleration to 0.7%.

The economic burden is falling most heavily on developing, net energy-importing nations. Inflation across developing economies is forecast to climb from 4.2% to 5.2% this year, as spiraling transport, fertilizer, and import costs erode real household income and constrain government fiscal spaces. While select African and Latin American oil exporters are seeing temporary revenue boosts from elevated crude prices, the broader macroeconomic landscape is plagued by tightening financial conditions. Sovereign debt yields are climbing globally, with U.S. 20-year and 30-year Treasury yields touching multi-decade highs near 5.1% as investors price in a "higher-for-longer" monetary stance from the Federal Reserve to combat this renewed commodity inflation.

Financial institutions and regulatory groups are already shifting focus to contain the systemic risks of a prolonged slowdown. While the International Monetary Fund (IMF) noted cautious market relief following the recent bilateral summit between U.S. President Donald Trump and Chinese President Xi Jinping in Beijing, officials emphasize that trade stability alone cannot offset localized energy shocks. Furthermore, the Financial Stability Board (FSB) and G7 finance ministers meeting in Paris this week are sounding alarms over secondary vulnerabilities, notably the rapid expansion of opaque private credit markets and AI-accelerated cyber threats to cross-border banking systems. As supply lines remain strained, central banks are left with minimal room to maneuver, balanced precariously between fighting stubborn energy-driven inflation and preventing a broader economic contraction.