By

By - 151

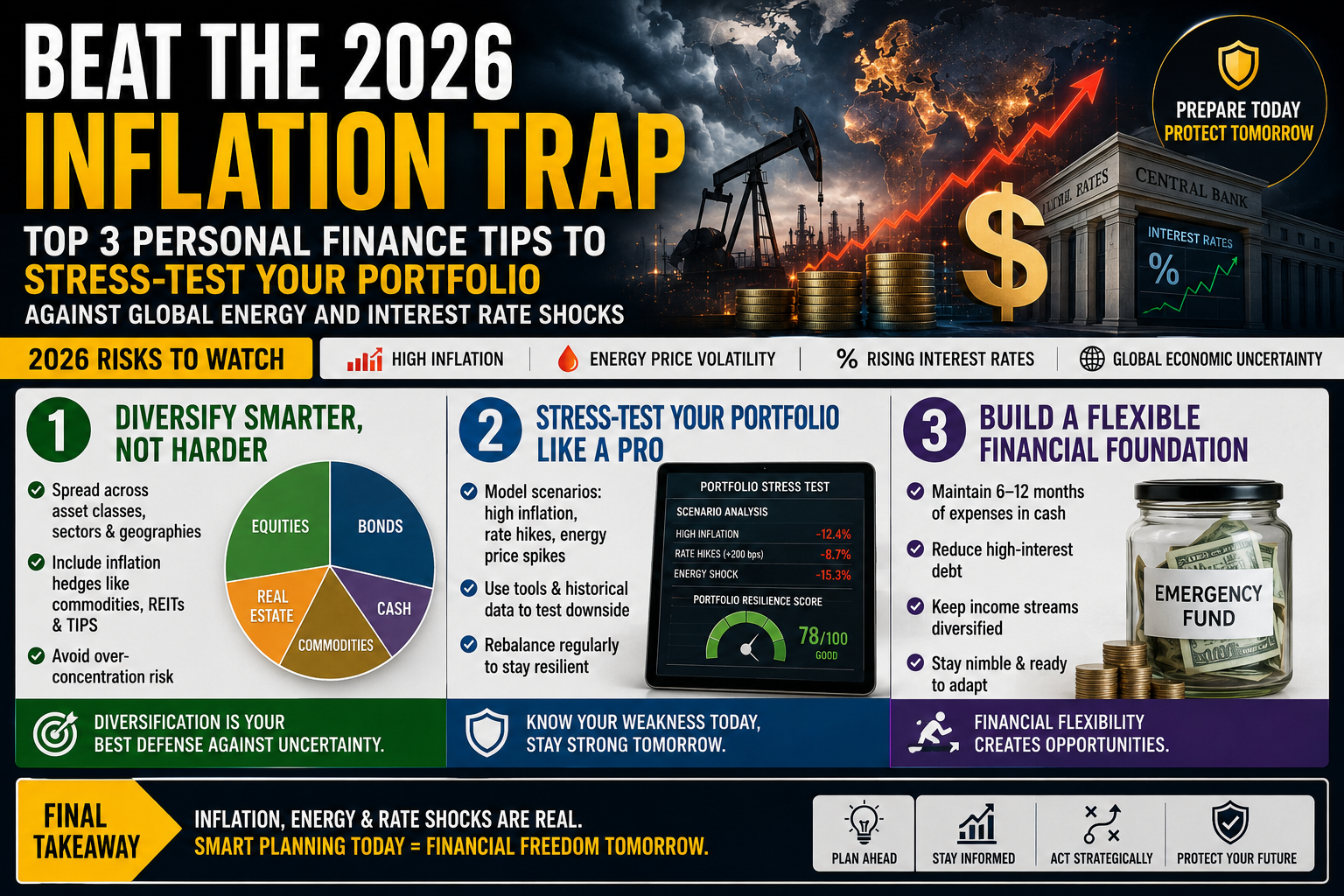

Top 3 Personal Finance Tips to Stress-Test Your Portfolio Against Global Energy and Interest Rate Shocks

Finance

The Hidden Tax on Wealth: Navigating the 2026 Macroeconomic Crunch

The mid-way mark of Q2 2026 has brought severe macroeconomic hurdles straight to the household doorstep. With global energy supply constraints in West Asia pushing crude oil indexes consistently higher, headline consumer inflation in India has climbed to a sticky 5.8 percent—holding persistently above the Reserve Bank of India’s (RBI) ideal 4 percent target cushion. For the average earner, this means the cost of daily living, fuel, groceries, and services is quietly rising even if individual income streams remain entirely flat. Leading asset management institutions, including J.P. Morgan and Morgan Stanley, warn that traditional "parking strategies"—such as keeping heavy amounts of idle liquid capital inside standard bank savings accounts—are functioning as passive wealth eroders. When a savings vehicle yields an interest clip of only 3 to 4 percent while overall consumer price indexes rise at nearly 6 percent, your money is effectively losing purchasing power in real terms. Surviving this timeline demands a deliberate transition from baseline saving to proactive portfolio protection.

Tip 1: Prioritize Real Returns and Rotate Into Inflation-Beating Assets

The primary rule of financial survival in late May 2026 is to aggressively evaluate every investment based on its true real return rather than its nominal paper rate. If a traditional Fixed Deposit (FD) guarantees a steady 6 percent return, a matching inflation print of 6 percent means your net wealth creation is mathematically zero. To break free from this neutral trap, shift a portion of your long-term capital into growth assets that historically outpace currency devaluations. Disciplined exposure to diversified equity mutual funds, hybrid allocation funds, and systematically managed small-cap or mid-cap baskets provides the necessary equity compounding to protect long-term purchasing power. Concurrently, ensure a portion of your wealth is allocated to digital gold or sovereign gold bonds; gold functions as an exceptional, uncorrupted hedge against global geoeconomic fragmentation and sudden maritime supply blockades.

Tip 2: De-Risk Floating Debt Liabilities Against Extended Interest Rate Peaks

Because sticky core and headline inflation pressures remain highly active worldwide, central banks are keeping their policy stances decidedly restrictive. Financial markets expect the Federal Reserve and the RBI to keep benchmark interest rates paused at elevated peaks throughout the remainder of 2026, eliminating any immediate hopes for cheap borrowing. For retail consumers, this translates directly to heavier burdens on Equated Monthly Installments (EMIs), particularly across home, vehicle, and floating-rate personal loans. If you are currently juggling floating-rate debt, execute an immediate financial diagnostic. Audit your loan terms to determine how many tenure extensions your lender has quietly tacked on to absorb rate spikes. Whenever possible, use mid-year bonuses, business dividends, or non-essential cash buffers to execute structured principal prepayments. Lowering your underlying debt baseline not only shields your monthly cash flow from future interest adjustments but saves your household from hundreds of thousands of rupees in compounding long-term liabilities.

Tip 3: Construct an Elastic Budget and Implement Automated Over-Indexing

The final column of an unshakeable 2026 wealth blueprint involves rebuilding your operational cash flow to handle modern price shocks gracefully. Review your monthly family expenses and construct a highly detailed, updated budget grounded entirely in today's realistic price thresholds rather than historical baselines. Identify and aggressively pause non-essential discretionary costs—such as duplicate digital streaming subscriptions, premium lifestyle upgrades, or heavy convenience app ordering fees. To counteract the steady creep of lifestyle inflation, configure your banking application to execute an automated annual step-up on all active Systematic Investment Plans (SIPs). Automatically raising your monthly investment contributions by 10 percent every year effectively forces your savings velocity to outrun the general rise of external living costs. By combining strict debt elimination with inflation-linked asset allocation and disciplined, automated investing, you can confidently turn a highly volatile macroeconomic storm into an organized era of generational wealth creation.