By

By - 118

Sensex and Nifty Bounce Back as India VIX Plummets and Government Announces Historic PPI Shift

Finance

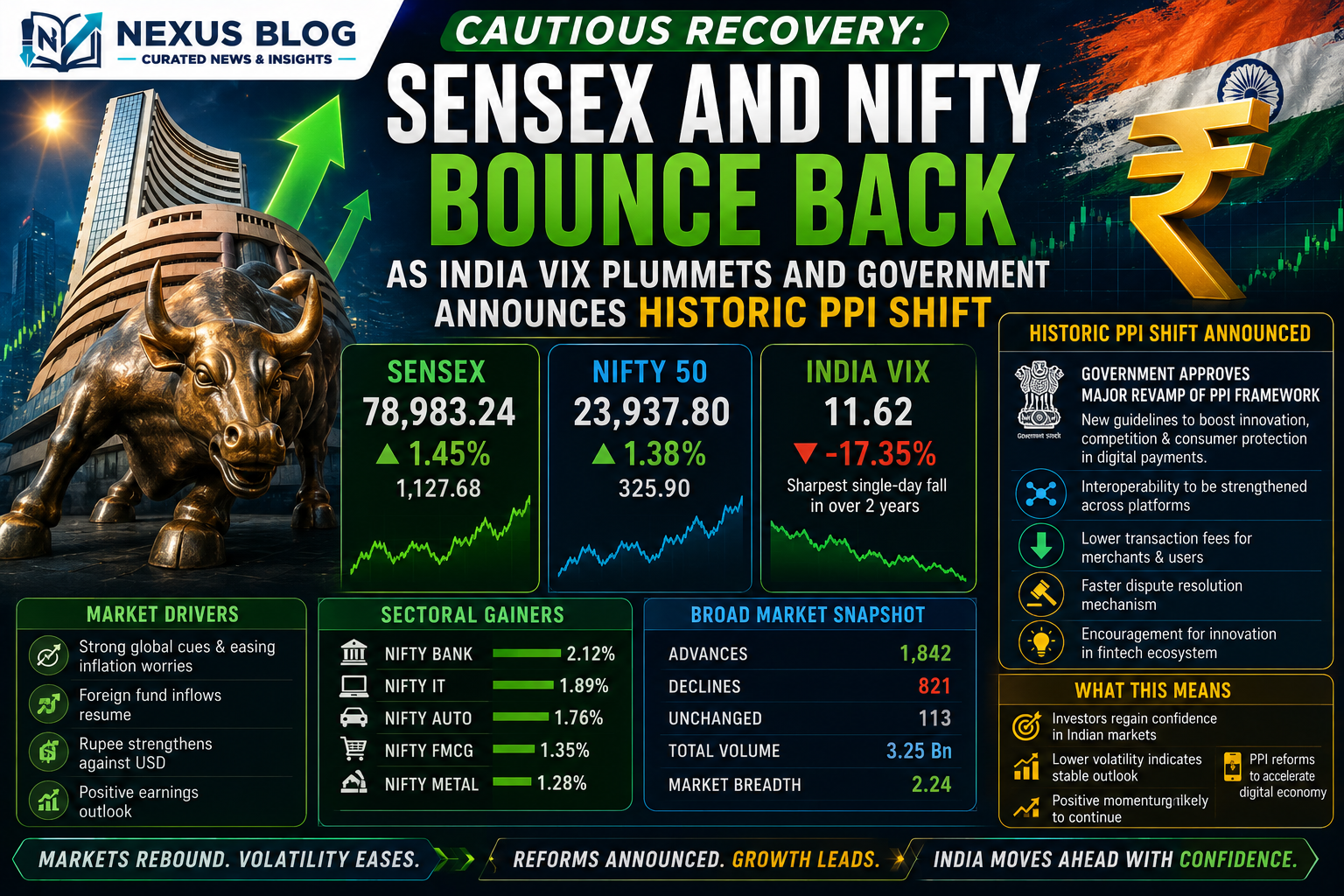

The Indian equity markets are witnessing a measured, highly cautious recovery during Thursday's trading session, following a week of erratic, headline-driven volatility. The benchmark BSE Sensex recovered from its deep intraday lows to edge over 100 points higher, hovering near the 74,380 mark, while the broader NSE Nifty 50 anchored itself comfortably around the 23,440 level. The defining highlight of today's market activity is the dramatic collapse of the India VIX (Volatility Index), which plummeted more than 18% to settle at 16.18 from a multi-week high of 19.85. This rapid cooling of market anxiety is heavily driven by short covering near weekly options expiry, combined with emerging signs of diplomatic de-escalation in West Asia. Reports of a conditional ceasefire agreement between Israel and Lebanon have successfully pulled Brent crude oil prices back below $97 per barrel, providing an immediate macroeconomic relief rally for energy-dependent emerging markets that were previously bracing for severe, imported inflationary pressures.

Sectoral divergence continues to define the broader market layout, creating a sharp contrast between resilient financial heavyweights and heavily battered technology counters. Leading the charge on the positive side is the Bank Nifty index, which scaled past the 54,260 level, vigorously supported by aggressive Domestic Institutional Investor (DII) buying and a fundamental tailwind of 16.2% year-on-year domestic bank credit growth—the fastest growth velocity recorded since mid-2024. Aligned sectors like Auto and FMCG are also capitalizing on the slide in crude prices, which directly lowers operational and raw material costs. Conversely, the technology domain remains under intense pressure; the Nifty IT index extended its pain from yesterday’s brutal 5.57% collapse. Market giants including TCS, Infosys, and LTIMindtree are facing persistent downward pressure as an aggressive mix of weak American Depositary Receipt (ADR) performance and corporate anxiety over localized artificial intelligence disruptions keep global funds highly risk-averse regarding traditional software outsourcing vendors.

Midday Sectoral Performance Matrix

| Index / Metric | Current Trading Level | Intraday Change (%) | Primary Market Driver |

| BSE Sensex | 74,380.50 | +0.13% | Recovering from intraday lows via banking support |

| NSE Nifty 50 | 23,440.05 | +0.15% | Supported by cooling crude oil prices |

| India VIX | 16.18 | -18.48% | Sharp drop in volatility due to options unwinding |

| Bank Nifty | 54,266.20 | +0.45% | Powered by robust 16.2% credit growth data |

| Nifty IT | 29,321.65 | -0.21% | Ongoing AI disruption fears and weak global tech cues |

Beyond the daily trading charts, the Commerce and Industry Ministry has dropped a monumental policy update that is set to permanently overhaul India's macroeconomic data architecture. The government has officially approved a structural framework to gradually phase out the legacy Wholesale Price Index (WPI) and completely replace it with a comprehensive Producer Price Index (PPI) system, updating the underlying base year to 2022-23. Financial analysts are widely celebrating this transition, as a modern PPI aligns India's inflation measurement with global best practices by tracking the actual prices received by domestic producers at the factory gate, entirely removing the double-counting of transport and trade margins inherent in the old WPI model. For corporate India and equity researchers, this data modernization will provide an incredibly precise, real-time look into manufacturing input stress, allowing the Reserve Bank of India (RBI) to formulate highly accurate monetary policies during highly volatile global commodity cycles.

Despite these constructive domestic regulatory upgrades, the immediate marketplace continues to face a stiff uphill battle against relentless global capital migration patterns. Foreign Institutional Investors (FIIs) have maintained their aggressive selling streak, dumping equities worth over ?5,616 crore in yesterday's session alone, as booming AI-led technology rallies in Taiwan and South Korea continue to pull global liquidity away from consumer-heavy emerging indices. However, leading global brokerages like JPMorgan urge market participants to maintain a long-term perspective, projecting that the Nifty could comfortably scale the 30,000 milestone by the close of the calendar year 2026 due to robust corporate earnings pipelines. For retail investors navigating this highly stock-specific landscape, the near-term strategy requires prioritizing balance-sheet quality and earnings visibility. As volatility indices stabilize, avoiding high-leverage momentum bets remains critical while global supply chains and West Asian geopolitical realities continue to search for a permanent baseline of stability.