By

By - 100

Finance

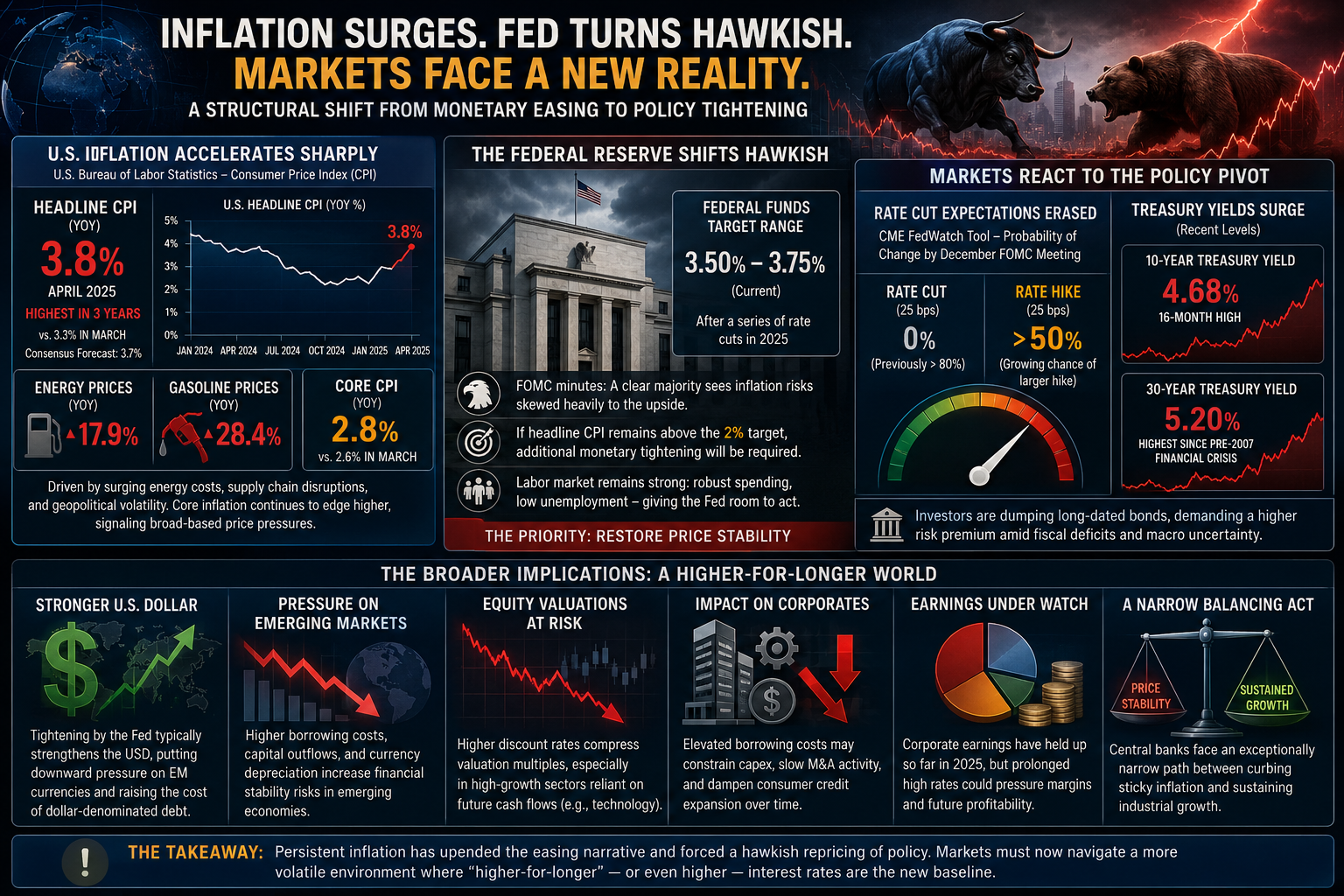

Global financial markets are facing an abrupt structural shift as persistent inflationary pressures disrupt the long-held narrative of monetary easing. According to the latest data released by the U.S. Bureau of Labor Statistics, the annual consumer inflation rate in the United States accelerated sharply to 3.8% for April, marking its highest level in three years and exceeding consensus market forecasts of 3.7%. This acceleration from March’s 3.3% reading represents a significant reversal from the steady downward trajectory observed throughout 2025. The resurgence is primarily attributed to a massive 17.9% year-on-year jump in energy costs—with gasoline prices surging 28.4%—compounded by escalating supply chain disruptions and geopolitical volatility affecting global commodity markets. Concurrently, core inflation, which strips out volatile food and energy sectors, edged higher to 2.8% year-on-year, indicating that price pressures are increasingly embedded across the broader domestic economy.

The unexpected resilience of inflation has dramatically shifted the policy outlook for the Federal Reserve. Having spent the latter half of 2025 implementing a series of rate reductions that brought the federal funds target range down to 3.50%–3.75%, the Federal Open Market Committee (FOMC) is now adopting a decidedly hawkish posture. The minutes from the central bank's recent policy meeting reveal that a clear majority of voting members view inflation risks as skewed heavily to the upside. Policymakers explicitly noted that if the headline Consumer Price Index (CPI) remains stubbornly above the long-term 2% target, additional monetary tightening will be required. The labor market's continued stability, characterized by robust consumer spending and low unemployment, provides the Fed with the necessary economic buffer to raise borrowing costs further without triggering an immediate recessionary spiral.

Fixed-income and derivative markets have responded swiftly to this policy pivot. According to the CME FedWatch Tool, financial instruments have completely erased previous expectations of further interest rate cuts this year. Instead, market probabilities now signal a greater than 50% chance of a 25-basis-point rate hike by the December meeting, with a growing minority of traders pricing in an even steeper increase. This recalibration has sent shockwaves through the bond market, where the benchmark US 10-year Treasury yield surged to a 16-month high of 4.68%, and the 30-year Treasury yield climbed to 5.2%—levels unseen since the preamble to the 2007 global financial crisis. Institutional investors are rapidly divesting from longer-dated sovereign debt, demanding a significantly higher risk premium to compensate for prolonged macroeconomic uncertainty and structural fiscal deficits.

The broader implications of a "higher-for-longer" or potentially rising interest rate environment extend well beyond domestic borders. A tightening cycle by the Federal Reserve typically strengthens the US dollar, exerting downward pressure on emerging market currencies and escalating the servicing costs of dollar-denominated debt globally. For equity markets, the reality of elevated discount rates threatens to compress corporate valuation multiples, particularly within high-growth sectors like technology that rely heavily on future cash flows. While corporate earnings have largely held steady through the initial months of the year, prolonged capital costs will likely constrain corporate capital expenditure, dampen mergers and acquisitions, and temper consumer credit expansion. As central banks worldwide navigate this volatile economic climate, the balance between curbing sticky inflation and sustaining industrial growth remains exceptionally narrow.