By

By - 124

Business

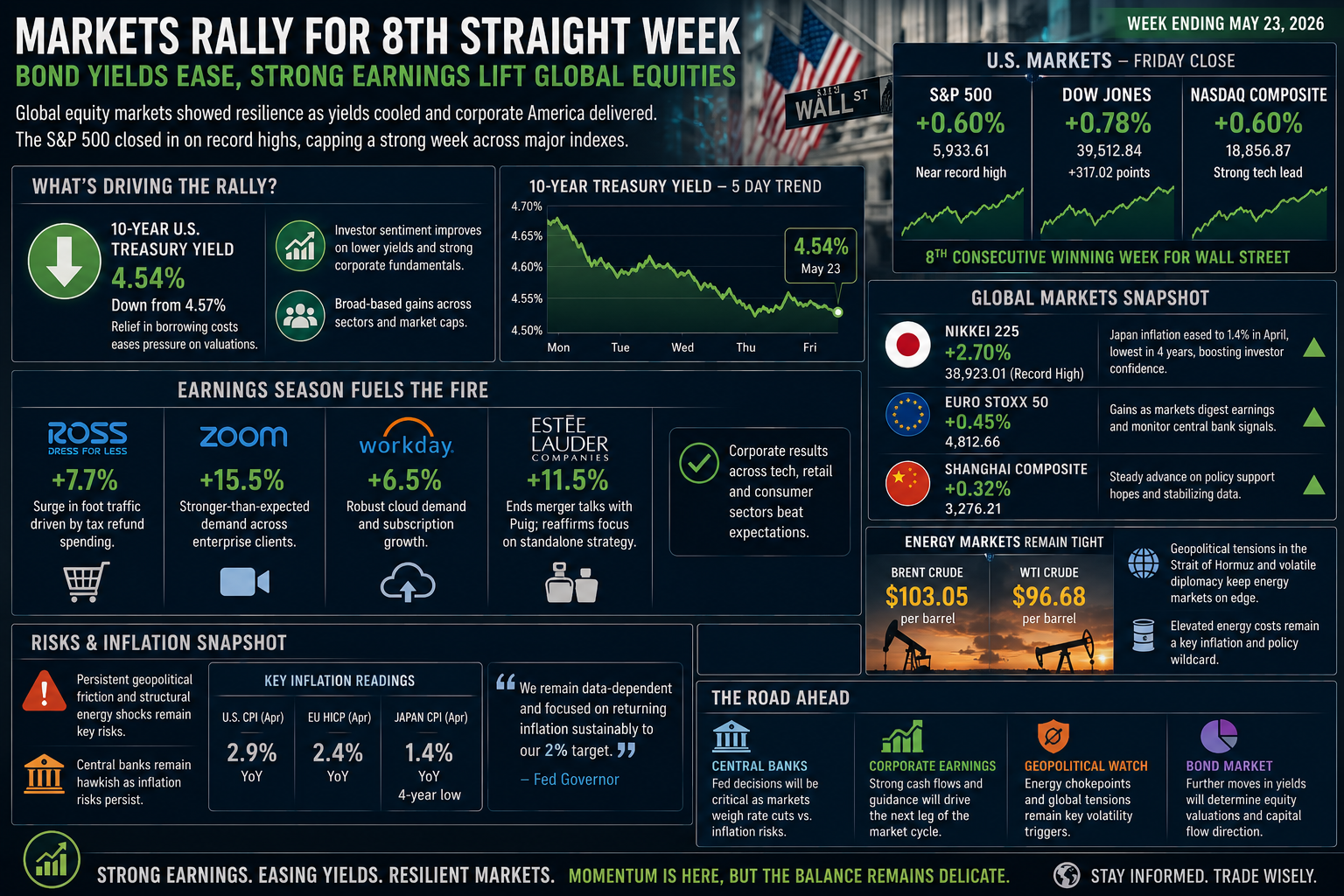

Global equity markets demonstrated notable resilience at the close of the trading week, driven by a welcome stabilization in the fixed-income sector and a robust wave of corporate earnings. On Friday, the S&P 500 climbed 0.6%, inching closer to the historic highs achieved earlier in the month and positioning Wall Street for its eighth consecutive winning week. Simultaneously, the Dow Jones Industrial Average surged over 300 points, while the tech-heavy Nasdaq Composite moved up symmetrically by 0.6%. This broad-based upward momentum reflected a significant shift in investor sentiment, primarily catalyzed by a drop in the benchmark 10-year U.S. Treasury yield to 4.54% from 4.57%. The minor contraction in borrowing costs successfully alleviated immediate valuation pressures on equities, allowing market participants to re-focus on strong domestic corporate fundamentals.

The rally was further sustained by an impressive corporate earnings season, particularly within the technology and retail sectors, which offset underlying macroeconomic apprehensions. Major consumer-facing companies reported quarterly figures that far exceeded conservative consensus estimates. Ross Stores saw its shares jump 7.7% following reported surges in customer foot traffic, a trend corporate leadership attributed to consumer spending linked with seasonal tax refunds. In the software and digital spaces, companies like Zoom Video Communications and Workday registered respective stock surges of 15.5% and 6.5% on the back of stronger-than-expected corporate demands. Additionally, corporate maneuvering provided individual stock highlights; for instance, Estée Lauder shares surged 11.5% after formally terminating exploratory merger considerations with Spanish beauty conglomerate Puig, reassuring shareholders of its independent strategic direction.

Despite the buoyant market metrics, trading volumes and forward projections remain tightly bound to persistent global geopolitical friction and systemic inflation. Energy commodities remained highly sensitive throughout the week, with Brent crude stabilizing at a lofty $103.05 per barrel and U.S. West Texas Intermediate hovering at $96.68. This elevated cost base stems from ongoing geopolitical anxieties surrounding the Strait of Hormuz and volatile diplomatic negotiations. While these factors have previously stoked fears of a hawkish pivot from global central banks, fresh data from key international allies provided a stabilizing counter-narrative. Notably, Japan’s Nikkei 225 surged 2.7% to touch a record high after national data indicated that domestic inflation had eased to a four-year low of 1.4% in April, confirming that localized inflationary pressures can cool despite stubborn global energy overheads.

Looking ahead, analysts maintain that market sustainability through the upcoming quarters will depend heavily on the next moves of major monetary authorities, such as the U.S. Federal Reserve. With hawkish rhetoric still originating from central bank governors due to persistent domestic inflation risks, the tension between strong corporate performance and high-for-longer interest rates persists. In the short term, however, institutional capital appears content to ride the momentum generated by corporate cash-flow health and the fractional decompression of the bond markets. As international markets prepare for the upcoming sessions, the delicate balance between structural energy shocks and resilient private sector earnings will remain the core focus of risk management desks worldwide.