By

By - 126

Finance

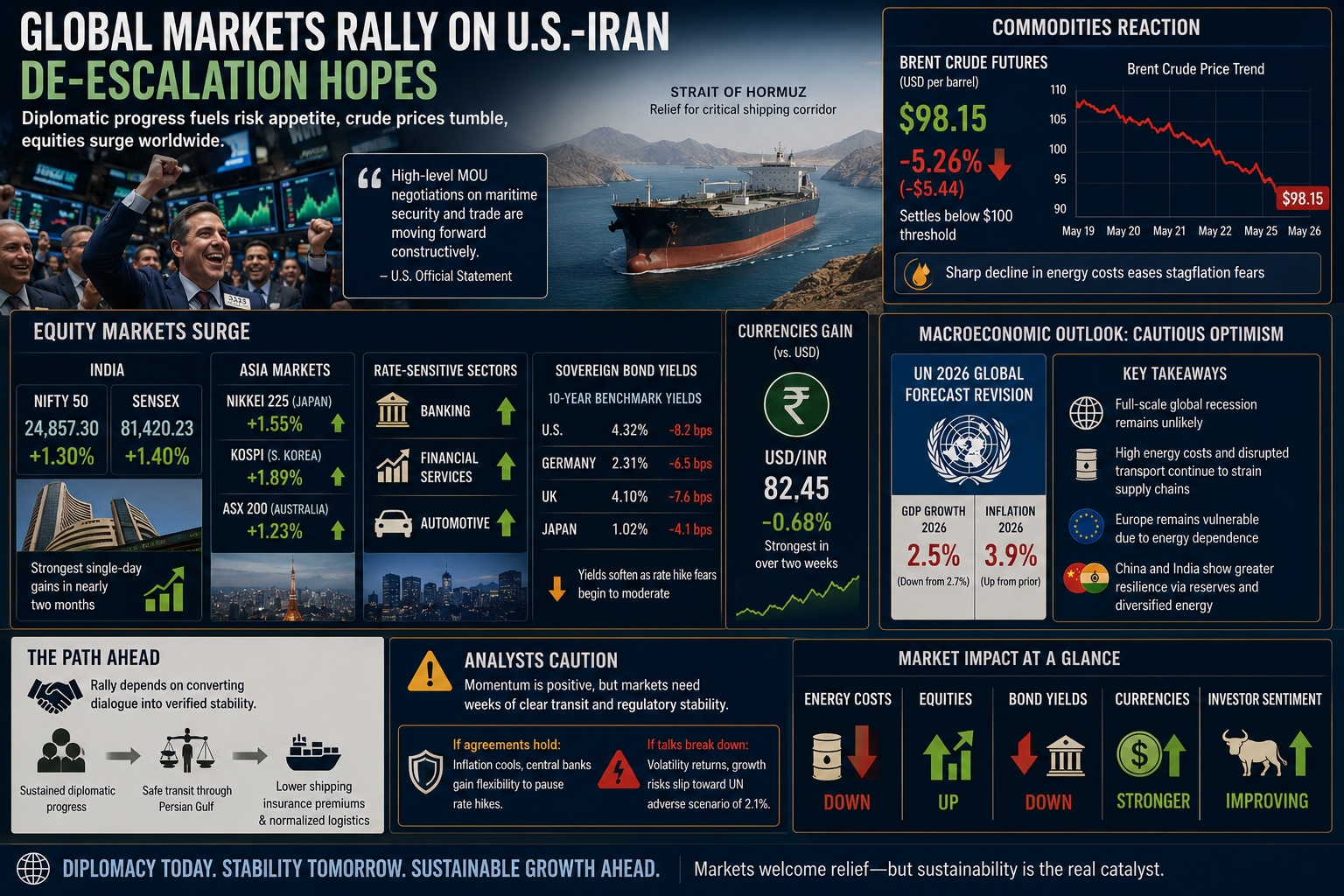

Global equity markets demonstrated a strong and broad-based recovery following signs of diplomatic progress between the United States and Iran. Sentiment was heavily buoyed by statements indicating that high-level memorandum of understanding negotiations regarding maritime security and trade were moving forward constructively. This potential de-escalation immediately relieved pressure on the critical Strait of Hormuz shipping corridor, which has been highly disrupted following earlier rounds of regional conflict. The most immediate and pronounced reaction occurred in the commodities sector, where Brent crude futures plummeted more than 5% to drop below the $100-per-barrel threshold, settling near $98 a barrel. The sharp decline in energy costs has provided a visual sigh of relief for international investors who had been pricing in prolonged, stagflationary energy disruptions.

The positive geopolitical momentum generated an aggressive wave of short covering and renewed risk appetite across major financial hubs. On domestic fronts, indexes such as India's NSE Nifty 50 and the BSE Sensex recorded their strongest single-day gains in nearly two months, surging by 1.3% and 1.4% respectively, heavily led by rate-sensitive sectors like banking, financial services, and automotive manufacturing. Concurrently, regional bank valuations and broader Asian indexes in Japan and South Korea posted robust advances. Sovereign bond markets also reflected this easing of risk, with benchmark 10-year yields softening globally as fears of immediate interest rate hikes by central banks began to moderate. Currencies sensitive to energy import costs, including the Indian rupee, strengthened against the U.S. dollar, marking their highest valuations in over two weeks.

Despite the near-term optimism on trading floors, the structural damage inflicted by recent geopolitical volatility continues to anchor macroeconomic projections. Just last week, the United Nations Department of Economic and Social Affairs revised its 2026 global gross domestic product (GDP) growth forecast down to 2.5%, down from an initial 2.7% estimate, while adjusting global inflation expectations upward to 3.9%. UN economists emphasized that while a full-scale global recession remains unlikely, the elevated cost of refined petroleum products and disrupted commercial transport networks continue to strain supply chains. The economic toll is distinctly uneven; European economies remain heavily exposed due to persistent reliance on imported energy, while larger developing economies like China and India have maintained comparative resilience by utilizing strategic reserves and diversified energy mixes.

Moving forward, the sustainability of this market rally depends entirely on translating diplomatic dialogue into verified regulatory stability. Market analysts caution that while the current momentum is incrementally positive, it will take several weeks of clear transit through the Persian Gulf for maritime shipping insurance premiums and supply chain logistics to fully normalize. If the draft agreements stabilize, the deceleration of energy-driven inflation could allow central banks greater flexibility in pausing their restrictive monetary cycles. Conversely, any sudden friction or breakdown in the ongoing diplomatic talks risks re-igniting volatility across raw material markets, potentially dragging global growth closer to the United Nations' adverse scenario baseline of 2.1%.